2023 – A period of recovery or the lead up to a market downturn?

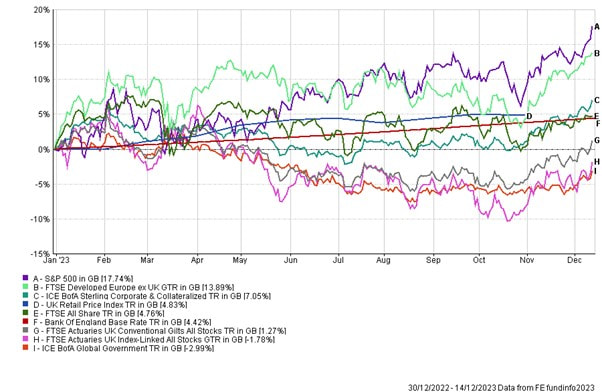

The graph below shows surprisingly robust equity performance in the back drop of a high inflation, high interest rate environment via the S&P 500 and the FTSE Developed Europe ex UK index. For the S&P 500, significant positive contributions have come from ‘The Magnificent Seven’ stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) which collectively make up more than 25% of the entire index.

In March, we saw the US Silicon Valley and Signature Banks collapse with Credit Suisse following suit in Europe which can be seen by the sharp dip in valuations for both the S&P and European indices. The impact was short lived and the fears of wider contagion were limited with the financial sector stabilizing shortly after.

When seeking to explain 2023’s buoyant economy, the long and variable lags of monetary tightening (the time it takes for interest rate hikes to take effect) are often referenced. So far in this cycle, these lags are proving to be longer and more variable than ever. An explanation partly lies in the resilience of the US consumer who built up a buffer of savings from fiscal support during the pandemic. These consumers have long been a growth engine for the global economy. There is a fear that this can’t last, especially with the pandemic-era stimulus reserves exhausted and recent consumption increasingly fueled by debt. [1]

Energy prices also fell from their highs in 2022 which helped reduce household bills for those across Europe and supply chain issues dating back from the pandemic were resolved so pent up consumer demand was freed up.

After a torrid 24 months there are shoots of recovery for UK government gilts with both Index Linked and Conventional Gilt indices showing movement in the right direction since mid-October. There will still be a long way to go to make up for the heavy losses in 2022 but as interest rates stabilise and inflation reduces further we expect to see continuing improvements in capital value for this asset class.

What’s in store for 2024?

Inflation and Interest Rates

With hopes that interest rates have now peaked in the major economies the next question is when are they going to start coming down again?

On 14th December 2023 Andrew Bailey re-iterated that although we’ve come a long way this year in the fight against inflation, there is still some way to go. The minutes from the Bank’s rate setters’ meeting also said that rates would need to stay higher “for sufficiently long” to return inflation to 2%. Indeed a number of fund houses have shared that they believe that the final push towards target inflation will be much more difficult. One reason is that services inflation has continued to be particularly sticky and both US and UK economies may have to see an increase in unemployment and reduced consumer and corporate spending before this starts to improve.

The European Central Bank also held rates at 4% in their last meeting and are holding firm that the rate needs to stay higher for longer. Inflation in the euro area is expected to decline gradually over the course of the year, before reaching the 2% target in 2025. It should be noted that signs of a mild economic slowdown have already appeared in the Eurozone area.

In the US, the Federal Reserve bucked the trend suggesting that interest rates could start to be cut next year if inflation continues to fall. This announcement saw a surge in markets with the Dow Jones closing a new record high (13th December 2023).

There is a spectrum of opinions by the fund houses as to when these cuts are going to happen, and by how much. The majority believe that the markets have priced in interest rate cuts in the second half of 2024 for the US Federal Bank and the Bank of England.

Geopolitical Risk

We look forward to the year when our outlooks don’t have to reference geopolitical uncertainty as a risk to the global economy and market behaviour. Alas this still has to be mentioned as 2/5ths of the world population will go to the polls over the next 12 – 18 months (with the US being the most noticeable for the markets). This isn’t traditionally the time for politicians to turn scrooge-like so in terms of macroeconomic framework, a combination of fiscal policy to fuel growth, coupled with monetary policy to act as a brake seems a distinct possibility. This could lead to market volatility as mixed signals between politicians and central banks affect sentiment.

It would also be remiss to mention the ongoing conflict between Russia and Ukraine which highlights how decades-old US led world order is fragmenting. The new, tragic conflict between Israel and Hamas further highlights the perilous nature of an increasing multipolar world. The ongoing troubles in the Middle East could affect global supply chains for fuel and goods which could create spikes in inflation. We also need to note the ongoing US-China tensions and the rise of political populism which could cause ongoing turbulence for economies and investors.[2]

What could this mean for the asset classes we invest in?

Many of the fund houses we use within our portfolios forecast an economic slowdown for 2024 – this could be a mild recession or just flat-lining growth. The economy has been resilient to this point but many investors expect the monetary policy tightening of the past two year to start to show up more in the real economy.

This would normally be bad news for Corporations with debt but many have used the last few years sensibly, taking advantage of ultra-low rates to issue debt at advantageous levels. This will mean that many companies will have more breathing space when it comes to needing to go back to the market for refinancing and the risk of default potentially lessened. [3]

A weaker economy and disinflation should be a supportive environment for government bonds. Fund managers see good opportunities for global fixed income including the UK. Income Yields are higher now than over the last decade and are starting to look attractive to investors who feel now is the time to become more defensive in their investment strategies as the concerns over economy resilience rise. [4]

This could prove a challenging environment for equities however there are still pockets of geographical regions and sectors where valuations currently look attractively priced (due to investor sentiment) but company fundamentals still look strong. This is where selecting quality companies can really help portfolios protect against a change in economic environment. [4]

The same can be said for Real Estate, where the outlook for the property sector appears gloomy to many commentators however, upon acknowledging that there are several factors posing significant challenges to real estate investors, there is also a belief that there are attractive opportunities to generate long term value.

Summary

In contrast to last year, there is much more of a consensus from the fund house economists as to their predictions for 2024, and although there are expectations for the global economies to see some downturn, more believe this will be ‘mild’ which is in a way more positive than in previous years.

We continue to expect pockets of volatility in markets, but also positivity in some sectors which is why we continue to use diversification as a tool in our portfolio construction. The more asset classes we hold, the better the chance we’ll see some upside in our portfolios.

But, perhaps the only certainty for 2024 is that it will turn out differently to how the fund houses expect. If the 2020’s have taught us anything it is to be ready for the unexpected!

References

[1] Janus Henderson Investors Investment Outlook 2024

[2] L&G CIO 2024 Outlook – Skirting risks, harvesting yields

[3] Royal London Outlook 2024

[4] HSBC 2024 Global Investment Outlook “A problem of interest - How rates affect investment strategy in 2024”

Risk Warnings

The graph below shows surprisingly robust equity performance in the back drop of a high inflation, high interest rate environment via the S&P 500 and the FTSE Developed Europe ex UK index. For the S&P 500, significant positive contributions have come from ‘The Magnificent Seven’ stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla) which collectively make up more than 25% of the entire index.

In March, we saw the US Silicon Valley and Signature Banks collapse with Credit Suisse following suit in Europe which can be seen by the sharp dip in valuations for both the S&P and European indices. The impact was short lived and the fears of wider contagion were limited with the financial sector stabilizing shortly after.

When seeking to explain 2023’s buoyant economy, the long and variable lags of monetary tightening (the time it takes for interest rate hikes to take effect) are often referenced. So far in this cycle, these lags are proving to be longer and more variable than ever. An explanation partly lies in the resilience of the US consumer who built up a buffer of savings from fiscal support during the pandemic. These consumers have long been a growth engine for the global economy. There is a fear that this can’t last, especially with the pandemic-era stimulus reserves exhausted and recent consumption increasingly fueled by debt. [1]

Energy prices also fell from their highs in 2022 which helped reduce household bills for those across Europe and supply chain issues dating back from the pandemic were resolved so pent up consumer demand was freed up.

After a torrid 24 months there are shoots of recovery for UK government gilts with both Index Linked and Conventional Gilt indices showing movement in the right direction since mid-October. There will still be a long way to go to make up for the heavy losses in 2022 but as interest rates stabilise and inflation reduces further we expect to see continuing improvements in capital value for this asset class.

What’s in store for 2024?

Inflation and Interest Rates

With hopes that interest rates have now peaked in the major economies the next question is when are they going to start coming down again?

On 14th December 2023 Andrew Bailey re-iterated that although we’ve come a long way this year in the fight against inflation, there is still some way to go. The minutes from the Bank’s rate setters’ meeting also said that rates would need to stay higher “for sufficiently long” to return inflation to 2%. Indeed a number of fund houses have shared that they believe that the final push towards target inflation will be much more difficult. One reason is that services inflation has continued to be particularly sticky and both US and UK economies may have to see an increase in unemployment and reduced consumer and corporate spending before this starts to improve.

The European Central Bank also held rates at 4% in their last meeting and are holding firm that the rate needs to stay higher for longer. Inflation in the euro area is expected to decline gradually over the course of the year, before reaching the 2% target in 2025. It should be noted that signs of a mild economic slowdown have already appeared in the Eurozone area.

In the US, the Federal Reserve bucked the trend suggesting that interest rates could start to be cut next year if inflation continues to fall. This announcement saw a surge in markets with the Dow Jones closing a new record high (13th December 2023).

There is a spectrum of opinions by the fund houses as to when these cuts are going to happen, and by how much. The majority believe that the markets have priced in interest rate cuts in the second half of 2024 for the US Federal Bank and the Bank of England.

Geopolitical Risk

We look forward to the year when our outlooks don’t have to reference geopolitical uncertainty as a risk to the global economy and market behaviour. Alas this still has to be mentioned as 2/5ths of the world population will go to the polls over the next 12 – 18 months (with the US being the most noticeable for the markets). This isn’t traditionally the time for politicians to turn scrooge-like so in terms of macroeconomic framework, a combination of fiscal policy to fuel growth, coupled with monetary policy to act as a brake seems a distinct possibility. This could lead to market volatility as mixed signals between politicians and central banks affect sentiment.

It would also be remiss to mention the ongoing conflict between Russia and Ukraine which highlights how decades-old US led world order is fragmenting. The new, tragic conflict between Israel and Hamas further highlights the perilous nature of an increasing multipolar world. The ongoing troubles in the Middle East could affect global supply chains for fuel and goods which could create spikes in inflation. We also need to note the ongoing US-China tensions and the rise of political populism which could cause ongoing turbulence for economies and investors.[2]

What could this mean for the asset classes we invest in?

Many of the fund houses we use within our portfolios forecast an economic slowdown for 2024 – this could be a mild recession or just flat-lining growth. The economy has been resilient to this point but many investors expect the monetary policy tightening of the past two year to start to show up more in the real economy.

This would normally be bad news for Corporations with debt but many have used the last few years sensibly, taking advantage of ultra-low rates to issue debt at advantageous levels. This will mean that many companies will have more breathing space when it comes to needing to go back to the market for refinancing and the risk of default potentially lessened. [3]

A weaker economy and disinflation should be a supportive environment for government bonds. Fund managers see good opportunities for global fixed income including the UK. Income Yields are higher now than over the last decade and are starting to look attractive to investors who feel now is the time to become more defensive in their investment strategies as the concerns over economy resilience rise. [4]

This could prove a challenging environment for equities however there are still pockets of geographical regions and sectors where valuations currently look attractively priced (due to investor sentiment) but company fundamentals still look strong. This is where selecting quality companies can really help portfolios protect against a change in economic environment. [4]

The same can be said for Real Estate, where the outlook for the property sector appears gloomy to many commentators however, upon acknowledging that there are several factors posing significant challenges to real estate investors, there is also a belief that there are attractive opportunities to generate long term value.

Summary

In contrast to last year, there is much more of a consensus from the fund house economists as to their predictions for 2024, and although there are expectations for the global economies to see some downturn, more believe this will be ‘mild’ which is in a way more positive than in previous years.

We continue to expect pockets of volatility in markets, but also positivity in some sectors which is why we continue to use diversification as a tool in our portfolio construction. The more asset classes we hold, the better the chance we’ll see some upside in our portfolios.

But, perhaps the only certainty for 2024 is that it will turn out differently to how the fund houses expect. If the 2020’s have taught us anything it is to be ready for the unexpected!

References

[1] Janus Henderson Investors Investment Outlook 2024

[2] L&G CIO 2024 Outlook – Skirting risks, harvesting yields

[3] Royal London Outlook 2024

[4] HSBC 2024 Global Investment Outlook “A problem of interest - How rates affect investment strategy in 2024”

Risk Warnings

- The value of an investment and the income from it could go down as well as up.

- All investing is subject to risk, including the possible loss of the money you invest.

- Past performance is not a reliable indicator of future results.

- Diversification does not ensure a profit or protect against a loss.

- Please remember that all investments involve some risk. Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income

- This communication is for general information only and is not intended to be individual advice. It represents our understanding of law and HM Revenue & Customs practice as at 2nd January 2024. You are recommended to seek competent professional advice before taking any action.